Why is the interest rate so low now? I've found out a very interesting history of the savings deposit rates offered by POSB which was known as Post Office Savings Bank in the past. The highest interest ever recorded was 9.5% on 1 August, 1981. I am not old enough to have experienced the history of interest rates in Singapore so i asked my parents and also searched on it in the internet.

My parents told me in those days, they had an average of 5-6% interest from the savings they put in the bank. Every year, they had hundreds or thousands of dollars in interest from the banks. My mum even said my grandpa always used the interest earned from savings in the bank to give red packets to us. We had very generous red packets from my grandpa on every Chinese new year at that time. That was in the late 1980s and early 1990s.

What happened to those days where we see high savings account interest in Singapore?

Below shows the Deposit interest rates in Singapore:

History of POSB interest rates

Here are the interesting facts i found out:

In 1965, interest rates was at 3%

In 1968, interest rates was revised upwards from 3% to 4%

In 1974, POSB was transferred to become part of the Ministry of Finance and Credit POSB Pte Ltd was established in the same year to provide custom-tailored loans relating to HDB housing ownership. POSB also raise the interest rate to 4.5% p.a. for deposit on 1st Jan, 5% in July and 8% in August.

On 1 September 1978, POSB introduced a 2-tier interest rate with a 5.25% p.a. for the first $100,000 deposit and 3.5% for the subsequent amount.

In 1980, it introduced the Passcard, and set-up the Principal Branch. On 1 May 1980, POSB revised the 2-tier interest rate upwards with a 7% p.a. for the first $100,000 deposit and 5% for the subsequent amount.

In 1981, its first Cash-On-Line ATM opened at the Newton Branch. On 1 July 1981, POSB revised the 2-tier interest rate upwards with a 9% p.a. for the first $100,000 deposit and 6.5% for the subsequent amount.

I remembered my dad had a very old POSB cash-on-line atm card but i just couldn't find any pictures on it. It was grey in colour and had a card holder also. Maybe some of you would remember that.

On 1 Auguest 1981, the interest rates on the first $100,000 was revised upwards to 9.5%. This was a historical moment as it was the highest interest rate every recorded.

The Post Office Savings Bank (POSB) was officially renamed as POSBank in March 1990. The word “Savings Bank” was dropped. On 1 June 1990, POSB adjusted the 2-tier interest rate upwards with a 4% p.a. for the first $100,000 deposit and 3% for the subsequent amount.

You would have realised that POSB has been paying higher interest rates on smaller amounts up to $100,000 and lower interest rates on subsequent amounts. This changed on 1 March 1998 due to the asian financial crisis. Commercial banks interest rates rose and this caused POSB to lose some of its bigger depositors. This prompted POSB to give higher interest rates of 4.125% to amounts above $100,000 and lower of 3.75% to amounts below $100,000

POSBank was fully acquired by DBS Bank on 16 November 1998. Witnessing the event were Finance Minister Dr. Richard Hu and DBS Bank Chairman Mr. S. Dhanabalan. This event marks the end of Savings Bank concept and welcome the new era of low interest loans in Singapore.

Mr. S. Dhanabalan, the Chairman of DBS Bank, declared that “POSBank cannot remain the way it is”. To start the ball rolling down hill, DBS announced on 18 November 1998 that POSBank Savings Account Balances, which is still tax-exempted, for the first $50,000 is at 2.25% p.a. down 0.5% and in excess of $50,000 at 2.25%. And swiftly on 10 December 1998 that POSBank Savings Account Balances for the first $50,000 adjusted downward to 1.5% p.a. and deposit in excess of $50,000 at 1.75%.

By year 2000, saving deposit interest rates dropped below 1% and has been even lower currently.

One good thing about the low interest rates on deposits was that loans interest rates also decreased significantly. Those who buy properties could borrow at a much lower rate which is also a cause of our sky-rocket housing prices currently as loans were very affordable.

Why we should invest?

At current low interest rates, our money becomes more and more worthless in the bank as inflation "eats" up a portion of our cash. Can we really feel the effects of inflation in our daily lives? If you ask the older generation, they would grumble about the higher prices today and compare the cheaper things they could buy back in the past. This is not their fault that they are complaining. They have live through the past and experienced things that we as younger people do not understand.

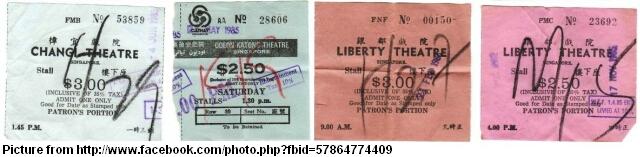

Let's look through at how much things cost in the past as compared to today. I found some interesting pictures on the internet. Pictures taken from remembersingapore.wordpress.com. Quite an interesting blog.

Bus tickets in Singapore. This one i remembered as i used to insert a transitlink card into the bus machine when i was in primary school and press a button for the correct fare and out comes a ticket like this. I guess this was much earlier than my time as its only 10cents per ticket. I remembered my student fare was 35cents at its cheapest for a non aircon bus. You should know how much prices are for public transport now.

Old movie tickets at $2.50 and $3 in 1985. Now? A weekday ticket at $7.50 and weekend ticket at $10.50. That's 3 times more expensive now.

HDB prices are the major increases. The current 4 room flat that i live in now cost $70,000 in the 1990s when my parents first bought it. Now it cost more than $300,000.

A bowl of fish ball noodle cost $2 in the 1990s. Now average cost around $3.

Will prices continue to rise? I'm sure it will unless our economy suffers a long recession and go into a deflationary mode. If this does happen, then we may lose our jobs too. We wouldn't want that to happen.

The purpose of me showing you the above price increase of different items is not to complain about the high cost of living but to bring to your attention that the same amount of money we have now will not buy us the same amount of things. In the 1960s and 1970s, people who have $1000 were considered those who are more well off. $1000 could buy you a lot of things and last you for months on food. Now, $1000 is nothing in our current economy. If we think that $100,000 is a lot for us now, it may be worth not much 10 years from now. With savings interest so low now, the need to invest become increasingly importantly. Or else, we will realise that our hard earned money saved is not enough for us to retire. Learn to invest and invest wisely.

Like my blog? Subscribe to receive updates of new posts by email.

Subscribe to SG Young Investment by Email

Read my below posts to find out more and get started in investing.

Related posts:

1. Investing basics - How do I start investing?

2. Investing Basics - Low Cost Index Fund investing (Passive Investing)

3. My views on the new POSB Invest-Saver

4. How to pick stocks (Part 1) - Economic Moats

No comments:

Post a Comment